The Shifting Sands of Stablecoins: A Duopoly in Decline

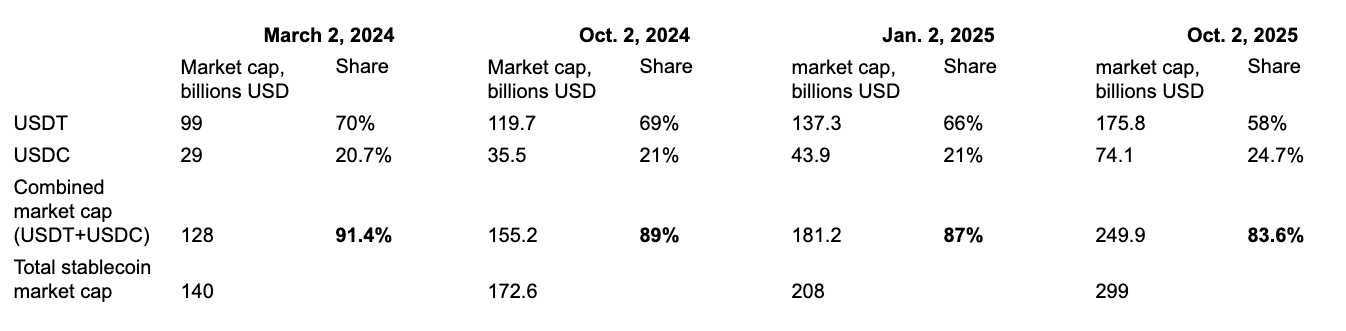

The stablecoin market, a cornerstone of the cryptocurrency ecosystem, is witnessing a notable transformation. The longstanding dominance of Tether’s USDT and Circle’s USDC, the two titans of the sector, is slowly eroding. Market data paints a clear picture: a combined market share that once peaked at over 91% has steadily declined, indicating a significant shift in the competitive landscape. This evolution presents both challenges and opportunities for existing players and new entrants alike.

Recent figures from platforms like DefiLlama and CoinGecko showcase the changing dynamics. While USDT and USDC continue to boast substantial market capitalizations, their collective hold on the stablecoin market is weakening. The decline, though gradual, is undeniable. This trend highlights a growing appetite for alternatives, fueled by a combination of factors, including the rise of yield-bearing stablecoins and the potential entry of traditional financial institutions.

Yield and Innovation: The Drivers of Change

One of the primary catalysts for this shift is the emergence of yield-bearing stablecoins. Projects like Ethena‘s USDe, which provides yield from crypto basis trading, have gained significant traction, demonstrating the appeal of passive income within the stablecoin space. This innovation allows users to earn returns on their holdings, a compelling proposition that challenges the traditional model. Competition among issuers to provide the most attractive yields is intensifying, potentially leading to a “race to the top” as projects strive to offer competitive returns.

The stablecoin market is no longer a two-horse race. A diverse array of stablecoins are emerging, each vying for a piece of the pie. These include offerings from established firms and innovative startups, all seeking to capture a share of the market. Regulatory developments, particularly those following the US GENIUS Act, are shaping the landscape. These regulations, designed to bring greater oversight to the industry, are also indirectly facilitating the entry of traditional financial institutions.

Banks Enter the Fray: A New Era Dawns

Perhaps the most significant development is the potential entry of banks into the stablecoin market. Driven by regulatory changes and the allure of new revenue streams, banks are exploring the issuance of their own stablecoins, often through collaborative ventures. Bank consortia, such as the one spearheaded by JPMorgan and Citigroup, could offer a formidable challenge to existing stablecoin issuers. These collaborations allow banks to pool resources, share expertise, and potentially create robust distribution networks.

“Newer startups will be able to undercut the major issuers on yield and create a race to the bottom (or realistically, the top) phenomenon.” – Nic Carter, Castle Island Ventures partner

The Future of Stablecoins: A Diversified Ecosystem

The decline of the USDT/USDC duopoly signals a move towards a more diversified and competitive stablecoin ecosystem. The interplay of yield-bearing products, regulatory developments, and the potential for bank-issued stablecoins promises a dynamic future. This evolution will likely result in a richer array of options for crypto users, leading to greater innovation and potentially, greater stability within the broader digital asset market. The coming years will be crucial in determining which players will ultimately thrive in this evolving landscape.