CARF: Crypto’s New Reporting Landscape Begins

The digital asset world is bracing for a significant shift. The Crypto-Asset Reporting Framework (CARF), spearheaded by the Organization for Economic Co-operation and Development (OECD), officially kicks off its data collection phase on January 1, 2026, in a staggering 48 jurisdictions. This global initiative aims to increase transparency and facilitate tax compliance within the burgeoning crypto space. For crypto users and exchanges alike, these new rules demand immediate attention and proactive measures.

What Does CARF Mean for You?

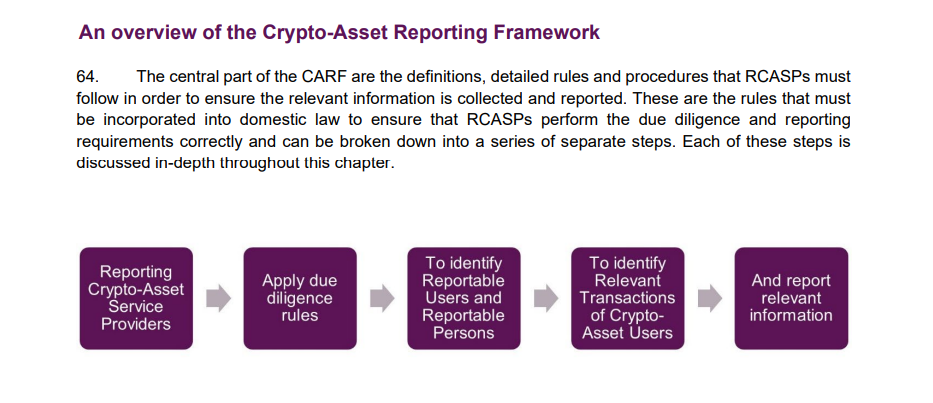

The impact of CARF is multifaceted. Essentially, the framework mandates that in-scope crypto providers – including exchanges and other platforms – collect comprehensive customer information, verify tax residency, and report users’ balances and transaction details to their respective tax authorities annually. These authorities will then share this data internationally, fostering a more coordinated approach to tax enforcement. The implications are far-reaching, potentially touching every facet of your crypto activities.

Exchanges: A Structural Overhaul

For crypto exchanges, complying with CARF necessitates a significant overhaul of existing infrastructure and processes. This isn’t just a cosmetic update; it’s a structural change that requires:

- Integrating CARF requirements into existing Know Your Customer (KYC) and Anti-Money Laundering (AML) protocols.

- Redesigning user onboarding to capture detailed tax residency information.

- Developing or upgrading reporting systems to meet stringent compliance standards.

This includes internal training, new governance frameworks, and tighter cooperation among compliance, engineering, and support teams, particularly for exchanges operating in various jurisdictions. The ability to navigate these changes successfully may become a competitive advantage, attracting users seeking compliant platforms within a rapidly evolving regulatory environment.

Retail Users: Increased Audit Risk

Retail crypto users, in the meantime, can expect a marked increase in audit risk rather than new taxes themselves. The framework doesn’t create new tax liabilities; instead, it strengthens the enforcement of existing rules. This means tax authorities will gain direct access to standardized, machine-readable data from exchanges, including those operating offshore, making it significantly easier to identify discrepancies between reported income and actual activity. Common issues include unreported offshore exchange activity, small disposals, and DeFi or NFT transactions not properly declared.

Navigating the Changes: Proactive Steps

Experts are urging both exchanges and users to take proactive steps now. While the initial reporting period begins in 2026, the data collected will inevitably be used to scrutinize past tax positions. For users, this means reviewing past crypto transactions, ensuring accurate reporting, and addressing any unresolved issues promptly, while voluntary disclosure options may still be available. For exchanges, early adoption and robust compliance strategies are key to mitigating regulatory and reputational risks. As the crypto landscape matures, understanding and complying with frameworks like CARF will become increasingly critical for sustained participation.

“While reporting begins in 2026, the data will inevitably be used to question historic positions where figures do not reconcile. Anyone with unresolved issues should be addressing them now, while voluntary disclosure is still available.” – The Bitcoin & Crypto Accountant.