The Stablecoin Revolution in Africa

Across the African continent, a quiet financial revolution is underway. From the bustling streets of Nairobi to the commercial heart of Lagos, stablecoins are no longer a niche interest but an increasingly vital tool for everyday financial life. Driven by the harsh realities of inflation, currency volatility, and the exorbitant costs of traditional remittances, stablecoins are providing a viable alternative for saving, making payments, and facilitating trade. This trend highlights a shift in how Africans are managing their finances, using technology to navigate complex economic challenges.

The Economic Imperative

The adoption of stablecoins in key African markets such as Nigeria and Kenya is directly linked to economic pressures. Inflation rates remain stubbornly high, eroding purchasing power, while currency fluctuations make it difficult for businesses and individuals to maintain financial stability. Furthermore, sending money across borders through traditional channels incurs significant fees, often exceeding 8% of the transfer amount. This contrasts sharply with the often lower fees associated with stablecoin-based remittances, providing a compelling incentive for their usage. The convenience of 24/7 transactions and the ability to easily convert stablecoins into local currencies through mobile money platforms further enhances their appeal.

How Stablecoins are Integrated

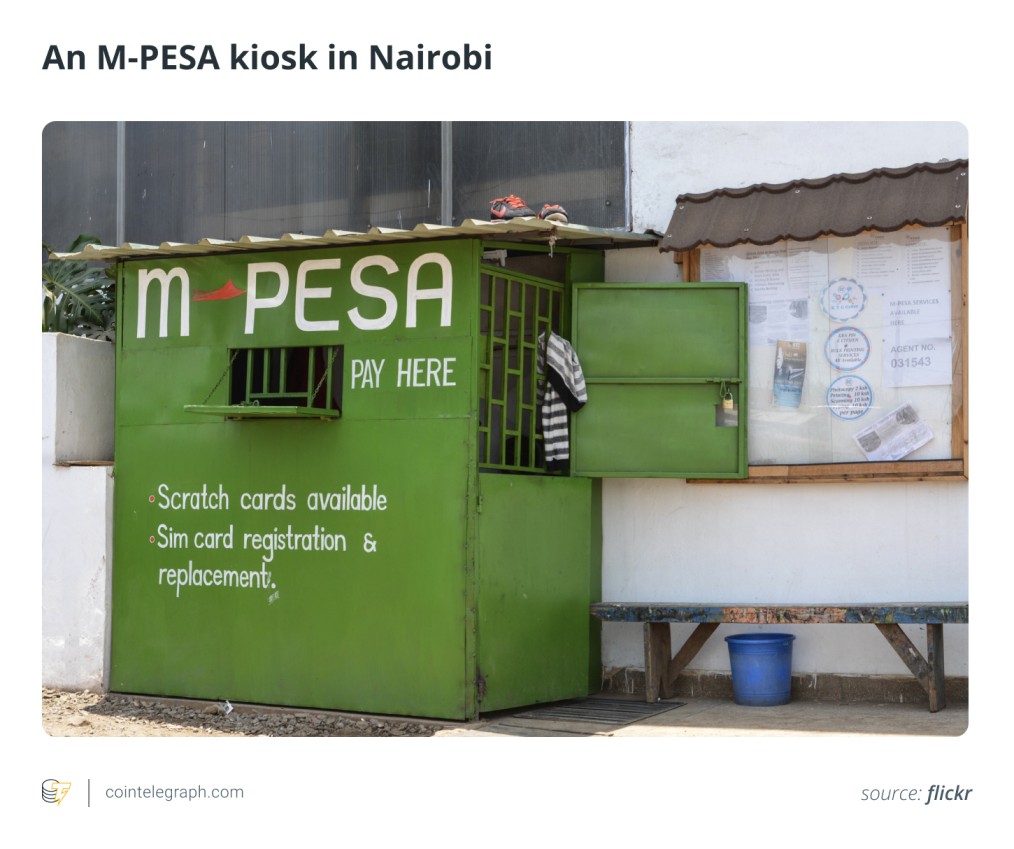

The success of stablecoins in Africa is largely attributable to seamless integration with existing mobile money infrastructure. Services like M-Pesa in Kenya and similar platforms across the continent allow users to easily convert stablecoins like USDC and USDT into local currencies. This integration makes stablecoins accessible and familiar to a broad audience. Companies like Kotani Pay, Yellow Card, and Chipper Cash are at the forefront of this movement, providing on- and off-ramps that link stablecoins to local payment networks. These solutions offer a faster, cheaper, and more reliable alternative to traditional financial services, particularly for cross-border transactions and small to medium-sized enterprise (SME) payments.

Navigating Regulatory Landscape

While the adoption of stablecoins continues to grow, the regulatory landscape remains in flux. Nigeria, for instance, has seen a significant shift in its stance, moving from outright prohibition to cautious permission and now towards stricter policing. These changes have included crackdowns on unauthorized platforms and increased scrutiny of digital asset service providers. Similarly, in Kenya, regulatory frameworks are evolving to address issues like taxation and licensing. This dynamic environment underscores the importance of staying informed and adhering to local regulations. The future of stablecoins in Africa hinges on the ability of regulators to balance innovation with the need for consumer protection and financial stability.

The Future of Digital Finance

The integration of stablecoins into the African financial ecosystem is more than just a technological advancement; it’s a testament to the ingenuity of individuals and businesses in adapting to economic challenges. Although challenges and risks exist, the trend of stablecoins is likely to continue. The focus on user-friendly interfaces, lower transaction costs, and secure systems will drive further adoption, shaping a more inclusive and efficient financial landscape for the continent. The key lies in balancing accessibility with the need for responsible innovation and effective regulatory frameworks.