The Dust Settles: Ripple‘s Legal Victory and the SWIFT Challenge

The long-awaited legal saga between Ripple Labs and the U.S. Securities and Exchange Commission (SEC) has finally reached its conclusion. This pivotal moment clears a significant hurdle for Ripple and its native cryptocurrency, XRP. But with the legal cloud lifted, the focus now shifts to a far greater challenge: disrupting the established dominance of SWIFT, the Society for Worldwide Interbank Financial Telecommunication, in the realm of global money transfers.

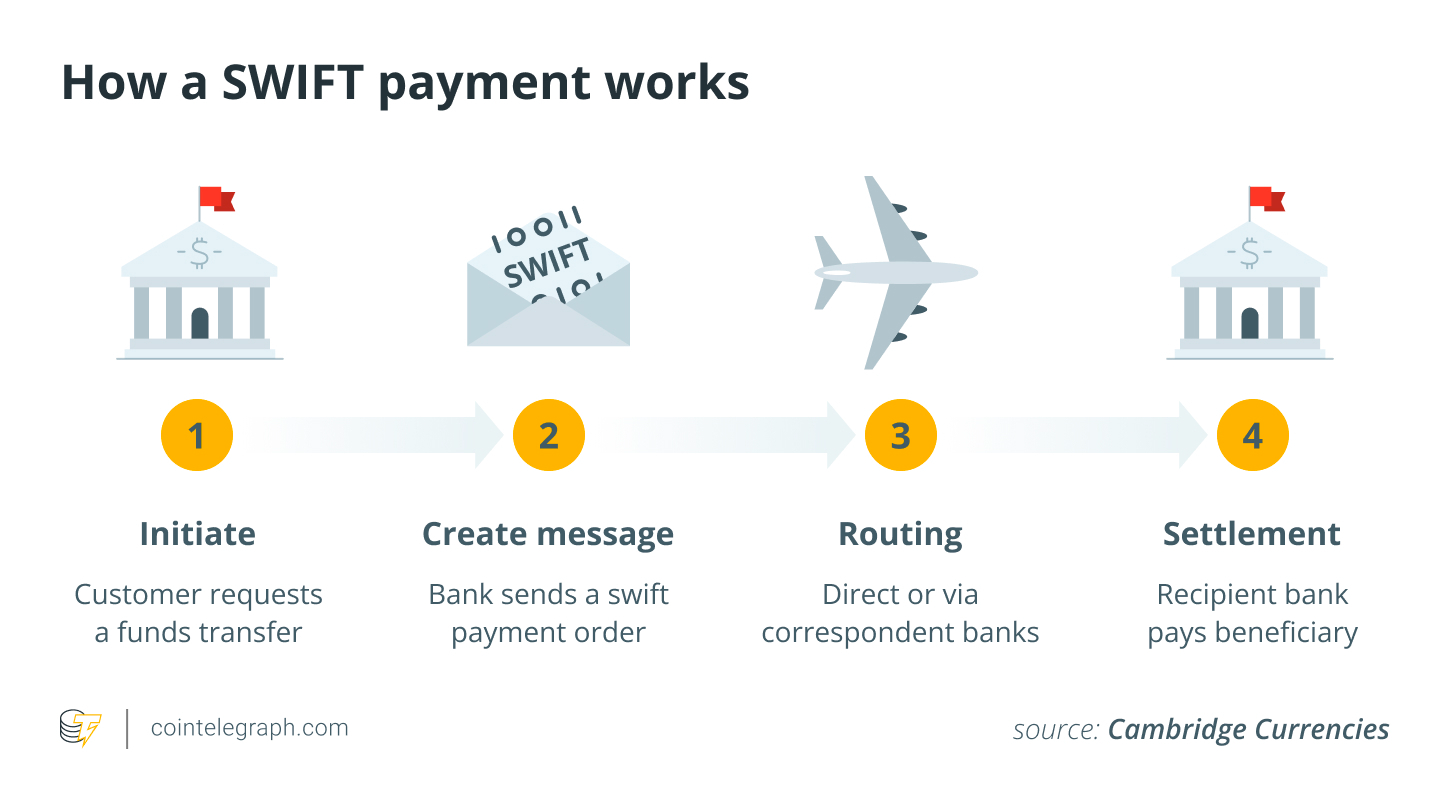

SWIFT‘s Reign and the Cry for Modernization

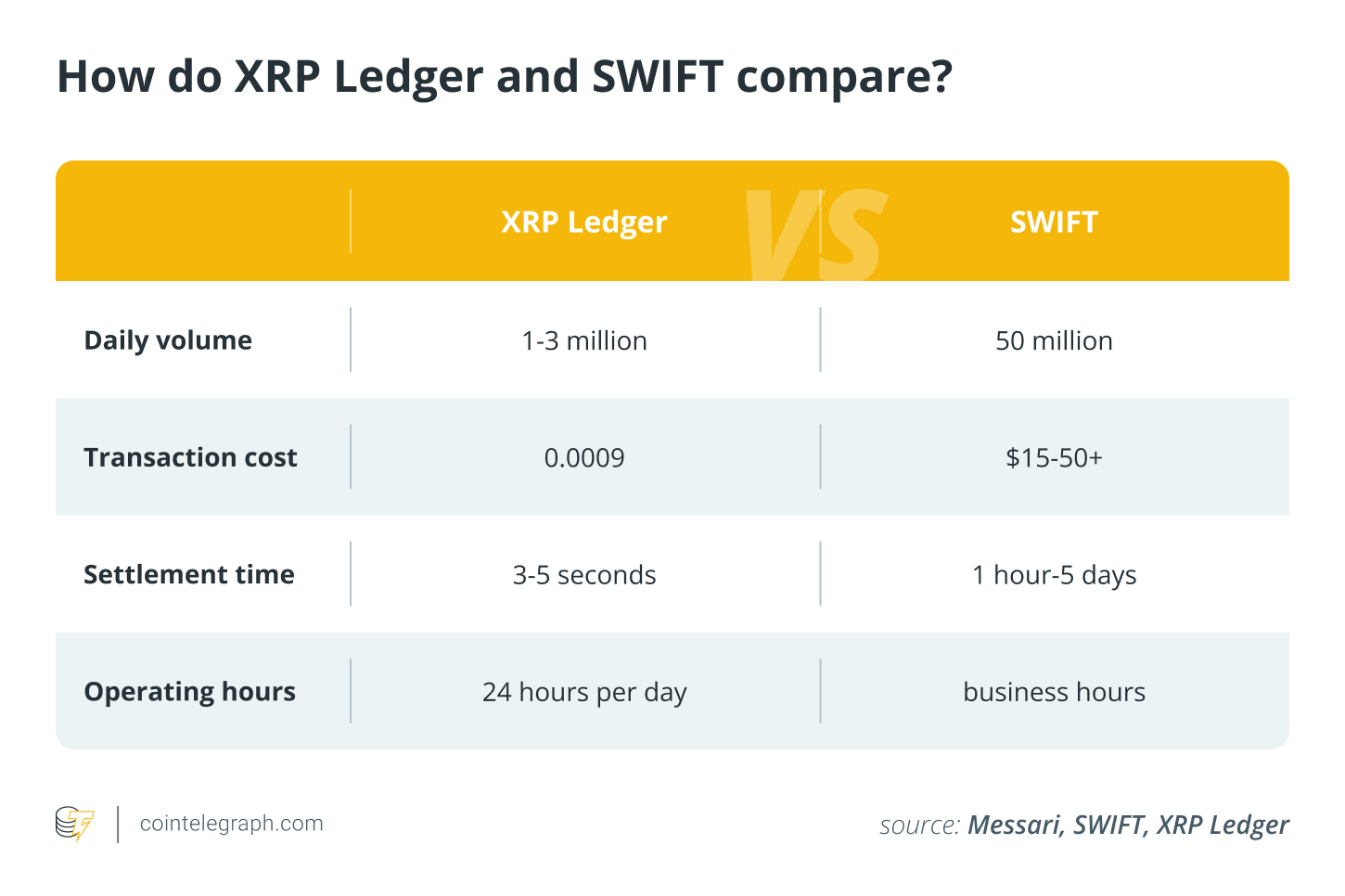

SWIFT, a cornerstone of international finance for over five decades, facilitates trillions of dollars in transactions annually. Yet, the system has faced criticism for its perceived inefficiencies. Transactions can be slow, incurring significant fees, and lack the transparency offered by more modern technological solutions. This is where Ripple and blockchain technology enter the picture. Proponents of blockchain, including Ripple CEO Brad Garlinghouse, argue that Ripple‘s technology offers faster settlement times, lower costs, and enhanced transparency – qualities that could potentially offer a compelling alternative to SWIFT.

Ripple‘s Advantages and Roadblocks

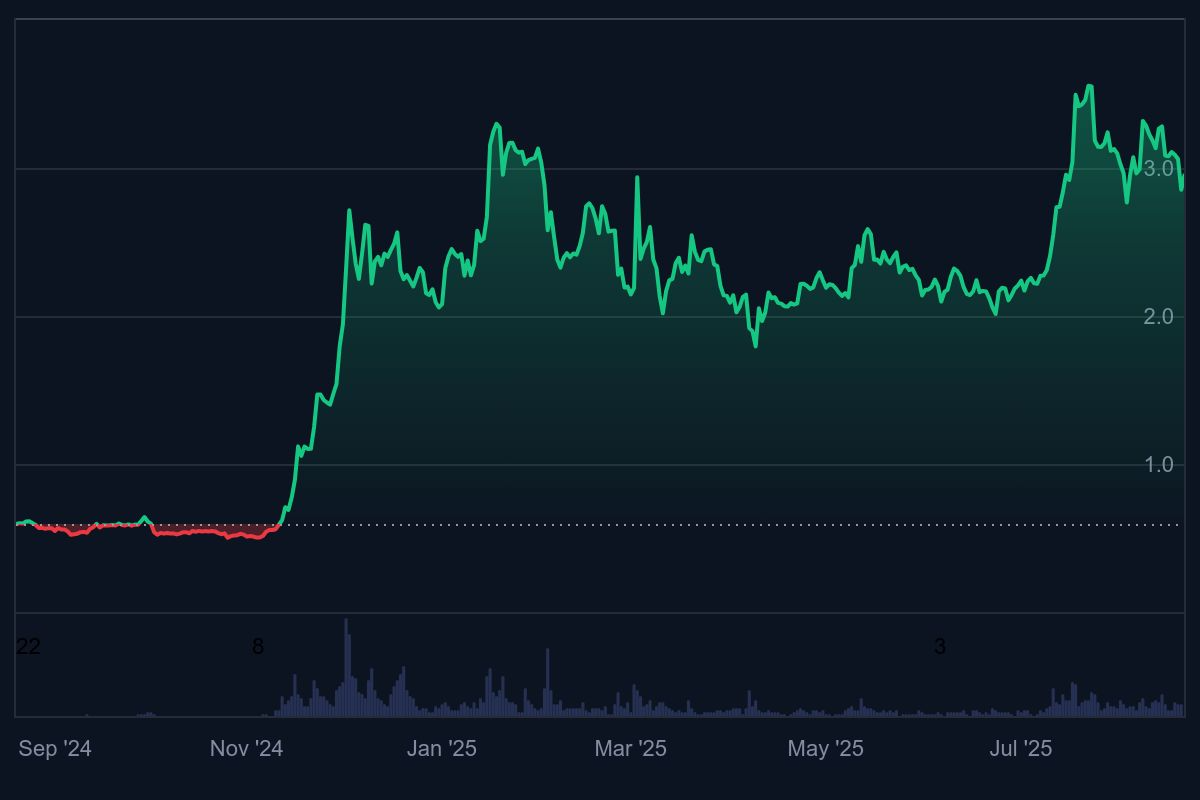

Ripple’s legal clarity, now bolstered by the SEC case resolution, is a significant asset. The ability to operate with increased certainty in a regulated environment provides a competitive advantage. XRP itself saw substantial price appreciation over the past year, indicating growing market confidence. However, replacing a network as deeply entrenched as SWIFT is no small feat. SWIFT’s ubiquity and the established comfort of financial institutions within its framework present formidable challenges. Banks are often wary of adopting new technologies, especially when these changes involve potentially significant operational risks and regulatory complexities.

The Path Forward: Bridging the Gap

Cassie Craddock, managing director for UK and Europe at Ripple, advocates for augmenting and modernizing existing financial infrastructure rather than outright replacement. This approach involves fostering interoperability and efficiency. Crucially, institutions need familiar tools, and regulatory clarity is essential. The introduction of stablecoins, like Ripple USD, aims to bridge this gap by offering digital assets pegged to traditional currencies, making them accessible and easily understood by traditional financial players. Regulatory changes, such as the GENIUS Act, provide a pathway for clarity and give institutions more confidence to adopt blockchain compliant technologies.

The Political and Regulatory Landscape

The current political climate also plays a role. US lawmakers show a preference for private stablecoins over a potential central bank digital currency (CBDC), offering opportunities for companies like Ripple. With the SEC’s investigation closed and a more crypto-friendly political landscape emerging, Ripple may find more favorable conditions to gain traction in the US. However, the road to disrupting SWIFT‘s dominance will not be straightforward. Ripple must convince financial institutions to adopt a new system, navigate complex regulations, and counter lingering concerns about the underlying liquidity of XRP.

The Future of Global Payments

The battle between Ripple and SWIFT highlights the broader evolution of the financial industry. As blockchain technology matures and regulatory frameworks become clearer, the potential for alternative payment systems to reshape the landscape remains substantial. While the entrenched position of SWIFT presents a formidable challenge, Ripple’s legal victory, technological advantages, and evolving regulatory landscape could pave the way for a significant shift in the future of global finance.